Current mortgage interest rates in Switzerland (2024)

|

5-year fixed rate mortgage |

10-year fixed rate mortgage |

SARON mortgage |

|

1.95% |

2,03% |

2.05% |

The above figures indicate current mortgage interest rates in Switzerland at the end of June 2024. The mortgage interest rates reflect the lowest published rates currently found in the market by our team of experienced mortgage brokers at Strike. Individual interest rates will vary depending on the borrower's circumstances and the lending institution. Contact an advisor now, free of charge and without obligation, to get access to the best rates and conditions on the market.

What are mortgage interest rates in Switzerland?

Mortgage interest rates reflect the cost of borrowing money to purchase a home. Mortgage interest rates in Switzerland are typically expressed as a percentage of the loan amount over a year.

So if a lender has purchased a home for CHF 1,000,000, the mortgage amount is CHF 800,000, and the mortgage interest rate is 2%, the annual interest rate payments will amount to CHF 16,000, or CHF 1333 per month.

Types of mortgage interest rates in Switzerland

In Switzerland, there are three principal types of mortgage products: fixed-rate mortgages, variable mortgages and SARON mortgages. Learn more about each of the mortgage types below, including their benefits and drawbacks:

Fixed-rate mortgage rates

Fixed-rate mortgages, known as Festhypothek or hypothèque à taux fixe in German and French, respectively, are by far the most popular mortgage option among Swiss property owners. This type of mortgage offers stability and predictability in financial planning. At the signing of the mortgage agreement, the mortgage interest rate is set based on current market conditions and the lender's risk assessment. This rate remains unchanged for the entire duration of the mortgage, making the monthly payments entirely predictable. Typical terms for fixed-rate mortgages in Switzerland range up to 10 years and longer.

Some of the main advantages of fixed-rate mortgages are:

- Fixed mortgage interest rates allow for precise financial planning over the entire term.

- The duration of the term can be negotiated to fit your needs.

- Fixed mortgage rates protect the borrower from rising market rates for many years.

The main disadvantages of fixed interest rate mortgages in Switzerland are:

- Fixed-rate mortgages are somewhat less flexible than other products.

- Homeowners can't benefit from falling interest rates.

SARON mortgage rates

SARON mortgage (formerly LIBOR mortgages) are the Swiss version of the tracker mortgage. In a SARON mortgage, the mortgage interest rate changes in line with current market interest rates. The mortgage interest rate of a SARON mortgage is composed of two parts: the SARON (Swiss Average Rate Overnight) base rate and a margin.

The SARON is a reference interest rate published daily by the Swiss National Bank (SNB). It reflects the average interest rate of overnight secured funding transactions in the Swiss Franc interbank market, providing a transparent and reliable benchmark for adjusting mortgage interest rates. On top of the SARON rate, banks add a customer-specific margin which reflects the bank's risk assessment. The base mortgage interest rate for each settlement period (typically 3 months) is calculated from the accumulated daily SARON rates.

Some of the main advantages of SARON mortgages are:

- In a very low interest rate environment, SARON mortgages tend to be the cheapest option.

- Should market rates fall over the term of the mortgage, borrowers will directly benefit from lower mortgage interest rates.

However, SARON mortgages have their drawbacks as well:

- The homeownership costs are unpredictable because they depend on future market interest rates.

- As a borrower, you bear the entire interest rate risk yourself.

Variable mortgage rates

A variable mortgage, or variable Hypothek, hypothèque à taux variable in German and French, respectively, is characterized by a variable interest rate, somewhat similar to a SARON mortgage. However, its mortgage interest rate is not tracking any specific market reference rate. Instead, it's the lending institution that sets the variable mortgage interest rate based on their own criteria.

Variable mortgage interest rates are generally much higher than comparable SARON or fixed-rate mortgage products; however, they have the most flexible contract terms of any mortgage, making them particularly suitable for interim financing.

Some of the main benefits of variable rate mortgages are:

- A variable rate mortgage can be redeemed at any time (subject to the notice period).

- There is no fixed term.

The main disadvantages of variable rate mortgages are the following:

- The mortgage interest rates are much higher compared to other mortgage types.

- The interest rates as set by the banks are not transparent because they are not directly based on market rates.

Current and past mortgage interest rates in Switzerland (graphs and trends)

Recent mortgage interest rate trends in Switzerland

After more than a decade of negative interest rates, 2022 marked a sharp turnaround in mortgage interest rates in Switzerland. Due to geopolitical uncertainty associated with the war in Ukraine, inflationary pressure from rising energy prices and the post-COVID shortage, fixed mortgage rates jumped by over 1.5% within a few months, suddenly making homeownership in Switzerland two to three times as expensive.

Initially, SARON mortgages were not affected by the rate hike, as the SARON rate closely tracks the SNB policy rate. However, as the SNB started raising its policy rate from -0.75% to 1.75%, SARON mortgage interest rates followed suit.

Since early to mid-2023, mortgage interest rates in Switzerland have gradually fallen to around 2%. Over the course of 2024, fixed-rate mortgage interest rates in Switzerland have been relatively stable, while SARON mortgages have become slightly cheaper following the SNB's rate cuts.

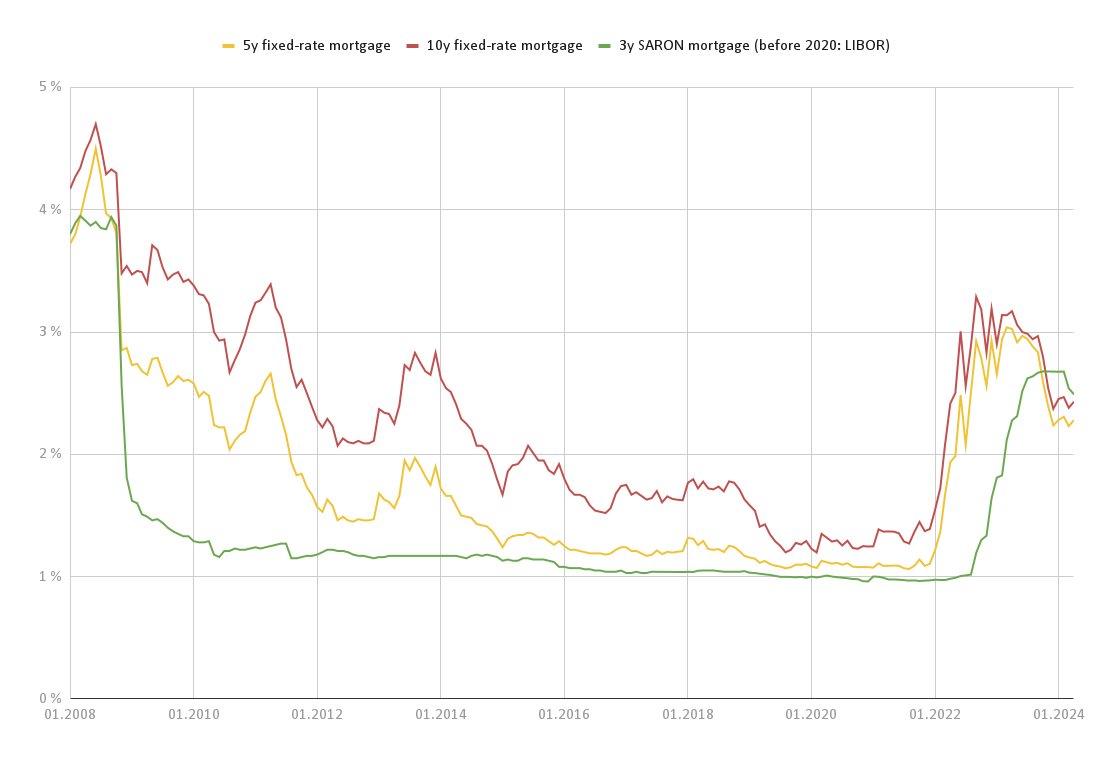

Trends in mortgage interest rates in Switzerland since 2008

The above chart illustrates the long-term development of mortgage interest rates in Switzerland, highlighting several distinct interest rate cycles:

High-interest period before 2008: In the years leading up to the global financial crisis, interest rates surged. Between 2004 and 2007, the Swiss National Bank (SNB) raised its policy interest rate ten times, from 0.25% to 2.75%. During this period, fixed mortgage interest rates peaked at over 4.5%.

Financial crisis: Following the global financial crisis, central banks worldwide lowered key interest rates to boost economic growth amid grim economic prospects. As a result, mortgage interest rates in Switzerland fell to record lows from around 2009 to 2021. Tracker mortgages (LIBOR/SARON) hovered around or even below 1% due to negative interest rates, and long-term fixed-rate mortgages in Switzerland were available at rates as low as 1%.

Developments in 2022: In the first half of 2022, fixed mortgage rates in Switzerland rose sharply. As the SNB began raising its policy interest rate to combat inflation, SARON mortgage rates followed suit. Mortgage interest rates in Switzerland peaked in April/May 2023. By early 2024, mortgage interest rates had declined to around 2% and have since remained stable.

Mortgage interest rates in Switzerland since 2020

|

5y fixed-rate mortgage |

10y fixed-rate mortgage |

3y SARON mortgage (before 2020: LIBOR) |

|

|

04.2024 |

2.28% |

2.43% |

2.49% |

|

03.2024 |

2.23% |

2.38% |

2.54% |

|

02.2024 |

2.31% |

2.47% |

2.68% |

|

01.2024 |

2.28% |

2.45% |

2.68% |

|

12.2023 |

2.24% |

2.37% |

2.68% |

|

11.2023 |

2.39% |

2.54% |

2.68% |

|

10.2023 |

2.59% |

2.8% |

2.68% |

|

09.2023 |

2.83% |

2.97% |

2.67% |

|

08.2023 |

2.88% |

2.94% |

2.64% |

|

07.2023 |

2.94% |

2.99% |

2.62% |

|

06.2023 |

2.97% |

3.0% |

2.52% |

|

05.2023 |

2.92% |

3.06% |

2.31% |

|

04.2023 |

3.03% |

3.17% |

2.28% |

|

03.2023 |

3.04% |

3.14% |

2.12% |

|

02.2023 |

2.94% |

3.14% |

1.83% |

|

01.2023 |

2.66% |

2.9% |

1.81% |

|

12.2022 |

2.93% |

3.19% |

1.64% |

|

11.2022 |

2.56% |

2.83% |

1.33% |

|

10.2022 |

2.79% |

3.19% |

1.3% |

|

09.2022 |

2.92% |

3.29% |

1.19% |

|

08.2022 |

2.5% |

2.89% |

1.02% |

|

07.2022 |

2.08% |

2.56% |

1.01% |

|

06.2022 |

2.49% |

3.01% |

1.0% |

|

05.2022 |

1.99% |

2.5% |

0.99% |

|

04.2022 |

1.94% |

2.42% |

0.98% |

|

03.2022 |

1.67% |

2.08% |

0.97% |

|

02.2022 |

1.37% |

1.72% |

0.97% |

|

01.2022 |

1.22% |

1.55% |

0.97% |

|

12.2021 |

1.1% |

1.39% |

0.97% |

|

11.2021 |

1.09% |

1.37% |

0.97% |

|

10.2021 |

1.14% |

1.45% |

0.96% |

|

09.2021 |

1.09% |

1.37% |

0.97% |

|

08.2021 |

1.06% |

1.27% |

0.97% |

|

07.2021 |

1.07% |

1.29% |

0.97% |

|

06.2021 |

1.09% |

1.35% |

0.98% |

|

05.2021 |

1.09% |

1.37% |

0.98% |

|

04.2021 |

1.09% |

1.37% |

0.98% |

|

03.2021 |

1.09% |

1.37% |

0.99% |

|

02.2021 |

1.11% |

1.39% |

1.0% |

|

01.2021 |

1.07% |

1.25% |

1.0% |

|

12.2020 |

1.08% |

1.25% |

0.96% |

|

11.2020 |

1.08% |

1.25% |

0.96% |

|

10.2020 |

1.08% |

1.23% |

0.98% |

|

09.2020 |

1.08% |

1.23% |

0.98% |

|

08.2020 |

1.11% |

1.29% |

0.99% |

|

07.2020 |

1.1% |

1.25% |

0.99% |

|

06.2020 |

1.11% |

1.3% |

1.0% |

|

05.2020 |

1.11% |

1.29% |

1.0% |

|

04.2020 |

1.12% |

1.32% |

1.01% |

|

03.2020 |

1.13% |

1.35% |

1.0% |

|

02.2020 |

1.07% |

1.2% |

0.99% |

|

01.2020 |

1.08% |

1.23% |

1.0% |

Predictions for mortgage interest rates in Switzerland

Most analysts currently expect the SNB to cut its policy rate to 1% by the end of 2024. This will mean that SARON mortgages will fall to around 2% given a typical margin of 1%. Fixed-rate mortgages are expected to remain around 2% in the medium term.

Factors influencing mortgage interest rates in Switzerland

Mortgage interest rates in Switzerland are shaped by a combination of economic, market, and policy factors. Understanding these influences can help borrowers anticipate changes and make informed decisions.

Swiss National Bank (SNB) policy

The SNB’s monetary policy is a primary driver of mortgage interest rates in Switzerland. By adjusting its policy interest rate, the SNB influences overall lending rates. When the SNB raises rates to control inflation, mortgage interest rates typically increase. Conversely, rate cuts aimed at stimulating the economy generally lead to lower mortgage interest rates in Switzerland. This is particularly the case for SARON mortgages, since the SARON reference rate closely tracks the SNB policy rate.

Inflation

Inflation rates directly impact interest rates. Higher inflation usually prompts the SNB to increase rates to cool the economy, leading to higher mortgage interest rates in Switzerland. Lower inflation often results in lower interest rates to encourage borrowing and spending.

Global economy

International economic events and trends can affect Swiss mortgage interest rates. This is particularly true of fixed-rate mortgages, whose mortgage interest rates tend to reflect long-term economic expectations.

How to get the best mortgage interest rates in Switzerland

Securing the best mortgage interest rates in Switzerland involves strategic planning and leveraging various opportunities to present yourself as a low-risk borrower to lenders. Here are some key tips to help you get the most favorable mortgage interest rates in Switzerland:

- Increase your equity: A larger down payment reduces the lender's risk and will lead to lower interest rates. Additionally, a smaller loan means reduced monthly payments, making the mortgage more affordable over time.

- Explore multiple lenders: Different lenders have varying criteria for mortgage approvals and interest rates. It's thus a good idea to shop around and compare offers from multiple banks and insurance companies to find the best rate and terms that suit your needs.

- Strengthen your application: Submitting a well-prepared and comprehensive application can ultimately secure you a lower mortgage interest rate. Ensure that all required documents are complete and well organized.

- Seek professional assistance: Working with a financial advisor or mortgage broker can be highly beneficial, as they have extensive knowledge of the mortgage market and access to a broad network of lenders. They can help prepare your application, negotiate on your behalf, and secure the best mortgage interest rates and terms.

Use our mortgage affordability calculator

Easily calculate the affordability of your mortgage loan in Switzerland using our free affordability calculator available here: https://strike-advisory.ch/en/real-estate-financing#affordability-calculator